{kind=link}

ICE, ICE baby

Copper prices retreated again on Monday to $3.09 a pound or $6,830 a tonne, bringing losses for the bellwether metal over the past week to nearly 6%. Two weeks ago copper touched the highest levels since January 2014.

Worries about the impact of a trade war between the US and China, which is responsible for nearly half the world’s industrial metal demand, are behind the pullback, but longer term the outlook for copper remains rosy.

While all the talk has been around booming demand for electric vehicles, a recent widely-read report by BMO Capital Markets argues that renewable energy infrastructure is the biggest single driver of global demand growth over the coming years.

The Canadian investment bank says the global push towards green energy necessitates “significant numbers” of small-scale electricity generation units to be connected to the grid.

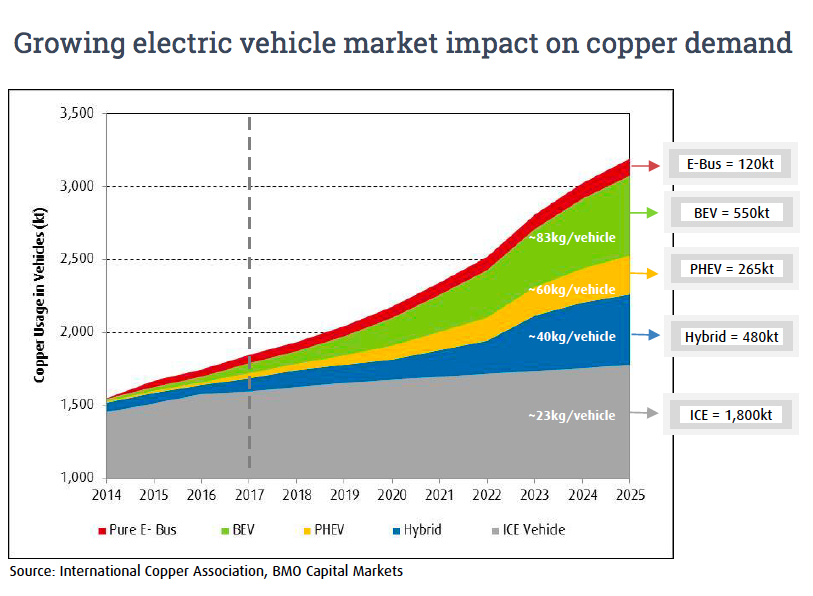

The additional copper required from the electrification of vehicles will catapult copper demand from the auto sector over the 3 million tonne level

Solar will add 2.5 million tonnes per year to global copper demand by 2025 and wind 1.85 million tonnes says BMO adding that offshore wind installations are particularly copper intensive, averaging over 9 tonnes of copper per megawatt.

Battery electric vehicles and plug-in hybrids require on average 3.6 times the amount of copper than an internal combustion engine (ICE).

Copper usage increases quickly as battery size expands – the copper in a full-electric SUV tops 100kg and in an e-bus it reaches 300kg.

BMO points out that despite the rapid transition to EVs, the traditional vehicle market is also still growing at a fast clip.

Currently ICE vehicles represent some 7% of copper demand and BMO forecasts sales growth of just over 10% by 2025 versus 2017:

This means that despite only containing ~23kg of copper each on average, OEMs will require ~1,800kt in 2025 to meet expected ICE vehicle demand.

However, it is the additional copper required (~1,300kt by 2025) from the electrification of vehicles (BEVs, PHEVs and Hybrids) that will catapult copper demand from the auto sector over the 3,000kt level.

Keep in mind that these figures represent BMO’s base case forecasts and risks are mainly to the upside.

Just this week the bank upped their forecasts for electric vehicle penetration thanks in part to changes made by Beijing to subsidies for EV and hybrids to favour longer range and therefore bigger batteries.

Global EV are up 70% through April compared to the same period last year and on pace to reach 2 million in sales this year vs 1.1 million in 2017 says BMO.

The house view is now 12% EV penetration (7% BEV, 5% PHEV) by 2025 which translates to 13.2 million units. One in four cars sold that year in China is predicted to be electrified.

The updated forecast adds an additional 125,000 tonnes to BMO’s prediction in the chart below for total demand from EVs of 3.32m tonnes.

Source: Renewable Energy: A Green Light to Copper Demand. BMO Capital Markets May 2018

The post Copper and cars: Boom goes beyond electric vehicles appeared first on MINING.com.

Source: Mining.com